The Economics of Aging(2024–2025)

This image was generated by AI and is provided for illustrative purposes only.

The economics of aging in the United States in 2024–2025 is a dynamic system where the final bill for care almost always exceeds the starting price seen in advertisements. Over the last two years, the market has become increasingly expensive as the senior population grows while the staff and infrastructure required to care for them face shortages. Additionally, rising requirements for quality and staffing ratios are driving up the cost of doing business.

The advertised base rate is just the starting point. Real expenses are determined by demographics, the labor market, geography, the specific community’s internal pricing model, and the surcharges that accumulate as a senior’s needs increase.

Macro Factors: Why Expenses Outpace Inflation

The market is being pushed upward by three key drivers acting simultaneously:

The Demographic Wave: A surge in the number of seniors requiring care.

Staffing Shortages: An acute lack of qualified caregivers and medical personnel.

Rising Standards: Increased regulatory requirements regarding how many staff members are needed per resident.

Consequently, prices are rising faster than most families anticipate, a trend affecting all levels of care.

National Price Dynamics

In 2024, prices increased across all care formats. Assisted Living is becoming noticeably more expensive because it operates 24/7 and relies heavily on a large workforce. Skilled Nursing remains the most expensive segment due to the complex medical processes involved.

The Market Logic is Simple: The higher a person's acuity (needs) and the more assistance they require daily, the faster the final bill grows.

Choosing a Format: Home vs. Facility

The financial gap between home care and facility-based living has narrowed. For moderate needs, partial home assistance can cost roughly the same as Assisted Living. However, once a person requires supervision for most of the day or 24/7 coverage, the "home" option becomes exponentially more expensive.

A Practical Example of Home Care Costs: It is crucial to understand how the budget is formed here. Providers like Senior Helpers of North Valley (serving Los Angeles and surrounding areas) cover a wide spectrum of needs—from regular housekeeping and personal care to Parkinson’s support and 24/7 companionship. In financial terms, this illustrates the transition of quantity into quality: home care evolves from "a few affordable visits a week" into a major monthly expense block, comparable to or exceeding facility costs, once a family needs to schedule staff in shifts.

Anatomy of the Bill: How the Price is Built

Understanding how the check is calculated helps avoid surprises. It is vital to distinguish between the base rate, the pricing model, and hidden surcharges.

What the "Base Rate" Actually Covers

The base rate typically covers the "hospitality" package:

Housing and partial utilities.

Meals and light housekeeping.

Access to activities and scheduled transportation.

Staff presence on-site (but not individual care!).

Key Clarification: Assistance with Activities of Daily Living (bathing, dressing, medication) is almost always added on top.

All-Inclusive

A single high rate covers housing and necessary care. Expenses are predictable, but the entry price is steep.

Tiered Model

Services are broken into levels assigned after a health assessment. The worse the health condition, the higher the monthly surcharge. This is the main source of price spikes.

Fee-for-Service

A minimal base rate, with every service (even help with buttons) listed as a separate line item. This makes the budget highly unpredictable.

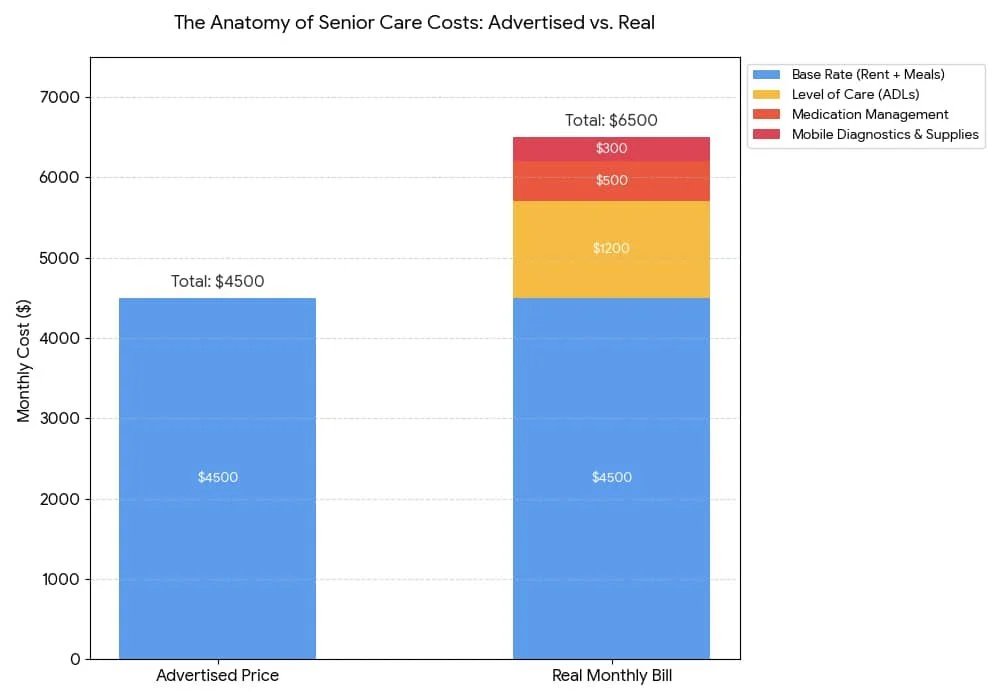

Figure 1. The Real Cost Gap. This chart illustrates how essential add-ons like personal care and medication management can increase the monthly bill by ~45% above the advertised base rate. Data Source: Estimates based on 2024 Genworth Cost of Care Survey and industry pricing averages. Chart generated for illustrative purposes.

Hidden Cost Drivers: Surcharges and Diagnostics

The difference between the ad and reality often lies in surcharges (second person fees, community fees, medication management). However, there is a category of expenses families often overlook: mobile diagnostics and logistics.

Instead of the complex logistics of transporting a mobility-impaired patient to a clinic, the market offers mobile services that become a separate line item:

Imaging: For example, Professional Imaging Network (Los Angeles) travels to the patient to perform X-rays and ultrasounds.

Lab Work: Sonic Diagnostic Laboratory (Los Angeles County) provides mobile phlebotomy and specimen collection.

In an Assisted Living model, such services often trigger a higher "Level of Care," while in a home scenario, they add regular bills that families rarely factor in when planning for "just a little help around the house."

Geography and Labor Risks in 2025

Location Dictates Price

National medians are only a rough guide. In some states, a specific level of care is considered "average," while in others, it is a "premium" product. Real estate costs, local wage levels, and the region's ability to retain staff all impact the price.

The Effect of New Standards (2025)

Federal staffing mandates for nursing homes, adopted in 2024, are rippling through the market:

Nursing homes are raising wages to meet quotas.

Assisted Living facilities are forced to compete for the same talent pool, driving their labor costs up.

If nursing homes limit admissions due to staff shortages, demand spills over into high-acuity Assisted Living, creating pricing pressure.

Forecast: In 2025, families will likely see rate increases above the historical average specifically due to this labor inflation.

Specialized Scenarios: Memory Care and Hospice

When needs extend beyond physical assistance, the economics of care change radically.

Memory Care: The Price of Safety

Dementia care is almost always more expensive than standard Assisted Living due to the need for a secure perimeter, higher staff-to-resident ratios, and specialized programming. Here, the example of Senior Helpers of North Valley fits naturally again: their specialized Alzheimer’s and Dementia Care programs focus on maintaining routine and dignity. This highlights that dementia is not just "another diagnosis" but a factor that alters the entire cost structure (requiring more trained humans) and the family budget.

The Value of Care Management

A quiet cost driver in dementia care is administrative inefficiency — poor coordination that triggers avoidable crises and wasted spending. Professional care management helps families stay on a clear, cost-smart path.

Dementia Partner in West Hills, CA is a good example. They don’t just “provide help”; they run the care strategy so families don’t pay for the wrong services or placements.

What care management usually does:

Assesses cognitive and daily-living needs

Builds a realistic care plan tied to the stage of dementia

Mediates family decisions

Screens and coordinates caregivers and providers

Guides placement to avoid expensive wrong moves

Provides on-call support during crises

Aligns care with legal/financial representatives

Bottom line: it shifts families from reactive spending to managed care.

Hospice Care: Shifting Focus

At a certain point, the priority shifts from rehabilitation to comfort. Integrating hospice care (such as Liem Hospice in Los Angeles County, which operates on a mobile basis) changes the economic model. While the medical component is often covered by insurance (like Medicare), the associated costs of round-the-clock monitoring and increased visit intensity restructure the family's financial planning.

Protection Strategy: Contracts and CCRCs

For long-term planning, CCRCs (Continuing Care Retirement Communities) exist. They operate on a "ladder of care" logic: entering via independent living and moving up to skilled nursing within the same campus. Finances here depend on the contract type: the higher the entrance fee, the better the protection against future price hikes.

How to Reduce Risks in Any Contract: The residency agreement is a financial instrument. It is critical to verify two clauses:

Rate Increase Mechanism: How often and by how much can they raise the rates?

Involuntary Discharge: Under what conditions can the facility terminate the contract (e.g., if the resident’s needs exceed the facility's license)?

Conclusion

Aging in the US in 2024–2025 is taking place against a backdrop of sustained structural cost growth.

The main takeaway for families is simple: The base rate is the minimum, not the final cost. The true cost emerges from the pricing model, regional factors, and surcharges—including mobile diagnostics, specialized dementia care, and intensified home support. The most rational approach is to calculate add-ons in advance, read the agreement as a strict financial contract, and understand that "home care" for high needs can eventually match the cost of a premium facility.

FAQ

1. Why is the final care bill always higher than the advertised price?

Because the advertised "base rate" covers only the hospitality minimum: housing, meals, light housekeeping, and access to common areas. Any personal assistance—from medication reminders to help with dressing—is considered an additional service. In the actual bill, these appear as separate line items or push you into a higher "Level of Care," which immediately increases the check.

2. Why are care costs rising faster than regular inflation?

Three factors are driving the market simultaneously:

Demographics: The number of seniors is increasing, driving up demand.

Labor Shortage: Finding nurses and caregivers is difficult, so facilities must raise wages to retain staff.

New Standards: In 2024, requirements regarding the number of staff per patient became stricter. To comply with the law, facilities are expanding their workforce and passing those costs on to clients.

3. Is it true that caring for an elderly relative at home is cheaper than in a facility?

This works only for low to moderate needs (a few visits per week). As soon as a person requires constant supervision or 24/7 assistance, home care becomes extremely expensive. For example, providers like Senior Helpers of North Valley ensure excellent quality of life at home, but round-the-clock coverage by qualified staff often exceeds the cost of living in a premium Assisted Living facility.

4. What payment models exist and which one is better?

There are three main models, and the choice depends on the person's health:

All-Inclusive: A high but predictable price. Beneficial if a significant amount of care is needed.

Tiered Model: Services are bundled into packages (levels). If health declines, you move to a higher level and pay more. This is the most common model.

Fee-for-Service: A low base rate, but every single action costs money. Highly unpredictable for the budget.

5. What hidden costs do families most often overlook when planning?

Expenses for logistics and mobile medicine. When a person finds it difficult to move, the family starts paying for home services that were previously received in a clinic for free or via insurance. This includes mobile X-rays and ultrasounds (e.g., from Professional Imaging Network) or home blood draws (provided by services like Sonic Diagnostic Laboratory). These sums accumulate quietly but significantly impact the budget.

6. Why does Memory Care cost more than standard living?

This is the price for safety and labor intensity. Patients with dementia require secure, enclosed perimeters to prevent wandering, as well as significantly more staff per resident to maintain routine and assist with basic tasks. It is a structurally different business process, so it is always more expensive.

7. What should I look for in the contract to avoid financial problems in the future?

Check two clauses carefully:

Rate Increases: How often and by how much does the facility have the right to raise prices (usually this happens annually).

Involuntary Discharge: Under what conditions of health deterioration will the facility state that they can no longer serve the resident and ask them to move out (e.g., if a feeding tube or complex medical equipment becomes necessary).

You May Also Like